The Inner Loop | n. 124

A coupla' predictions for 2021.

Australian Fintech and Startups

Slyp’s itemised digital receipts are now live within the NAB banking app. What an incredible achievement (and also exceptional user experience) for the NAB and Slyp partnership. Expect the other three to follow suit in 2021. Link

86400 launched shared accounts. Link

NSW’s Opal card will soon be offered as a digital card. Those who constantly lose their Opal cards (me) rejoice. Link

The Singapore Fintech festival happened this week, with a strong representation from Australia. I highly recommend going to this YouTube channel to watch 30 min ‘Ask Me Anything’ from some of the most prominent names in Fintech. Link

What, in your opinion, is the biggest thing to happen in Australian Fintech this year? Put your responses here and let’s get an end-of-year discussion happening!

Big Tech

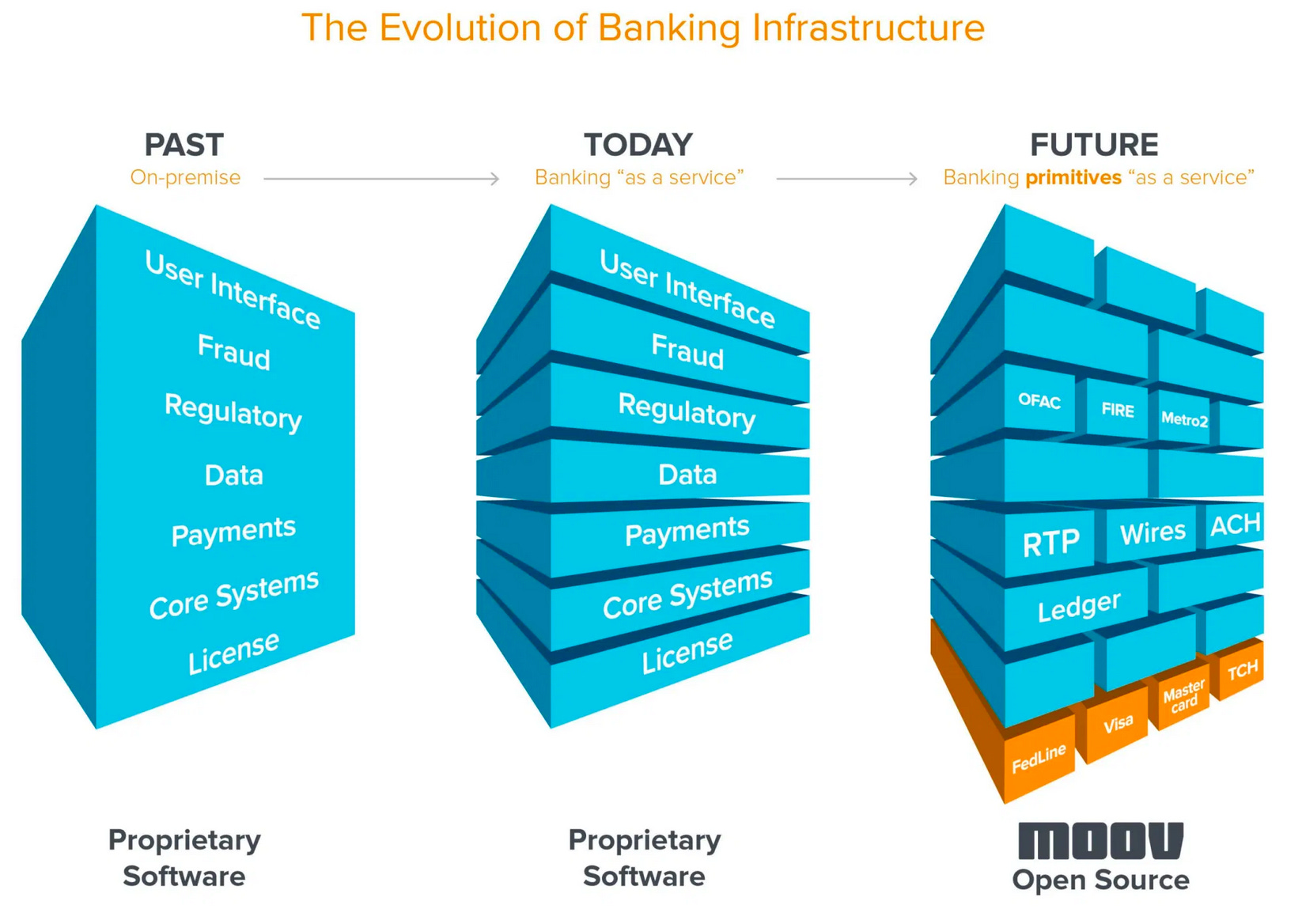

Source: a16z - “Investing in Moov”

Thought-provoking read: The evolution of banking infrastructure - from Past (‘on premise’), to now (‘Banking as a Service’) to the future '(‘Banking primitives as a service’). Aka, unbundle each service in a BaaS layer and use it as its own distinct module (I guess you could say, as the highest level of abstraction, that it’s a Product interpretation of how microservices work). Link

DoorDash’s IPO went through the roof. Link

Stripe announced ‘Stripe Treasury’. Something something every business becomes a bank. Link

Potpourri

Mt Everest grew by ~1m after surveyors from Nepal and China agreed to a new height. Link

Hilarious Twitter thread by ‘Sir Michael’ who satirises Facebook users. Link

Most prescient article of the year: “Coronavirus forces world’s largest work-from-home experiment” (published February 2nd). It’s almost eerie to read this thinking how much has changed since then. Link

Jimmy’s 2020 EOY Notes

Whew! What a year. I’ll be back and writing some time in mid January after the break. Before I head to the beach, I’m going to remind everyone what the three largest takeaways were from 2019 (from The Inner Loop #81) - (1) BNPL sector growth (2) IPO rollercoasters and (3) Neobanks and banking licenses.

I’d say in 2020, one of those still holds true - and that’s the growth in BNPL (both domestically and internationally). And, not so much purely growth, but more product diversification - specifically how BNPLs are moving into the cards space (or partnering with issuers), how Banks have started offering BNPL cards, and - what I think is most striking - is the partnerships that have emerged between Banks and BNPL. A number of pundits claim that Afterpay will be the ‘new Bank’ - but really, every company that provides a great customer experience will be a Bank. Barriers to entry for financial services are now lower than ever, and soon any company that is looking to offer any form of financial services can do so with ease (see Stripe Treasury for a B2B example that launched this week).

So, with that in mind, paired with a whole bunch of other things that happened this year, my predictions for 2021:

(a) QR codes in Australia will start to become the ‘new normal’ for payments. People actually know what a QR code is now thanks to COVID-19 and QR contact tracing in Australia. This created a drastic uptick in QR adoption and made people familiar with the fuzzy black-and-white-square-that-can-do-stuff. I think that, quicker than we know it, the inception point for purchasing will no longer be through a physical card, but through a QR. Bear in mind we are way behind Asia in this, where in many countries (Singapore, China, Japan) QR is the preferred way to pay. With the NPPA’s Mandated Payment Service (MPS), third parties will soon be able to initiate payments from Bank accounts. This completely disintermediates payment terminals and means that many transactions will be done phone-to-merchant. Interestingly, this means Point of Sale (POS) companies will be more relevant than ever to provide the QR (and, interestingly, they are the ones to thank for providing contract tracing measures quicker than the various Australian State Govts). Big caveat here: this is currently done through ordering apps e.g. Mr Yum & me&u - but widespread merchant adoption may not happen til 2022.

(b) BNPL will continue to boom in terms of product diversification. I’m exceptionally bullish on BNPL after the fairly-light-on ASIC report and the RBA’s lack of interest in changing the no surcharge rule. BNPL is both a consumer product (credit) and a merchant product (increased conversion) - but I think we will see the focus on the consumer product side increase - Afterpay will soon issue their own cards (if you open the app they even let you know of the limit they’ll offer you), and I think Zip’s next step is to partner with another Bank to offer some form of savings accounts. Money is now more liquid than ever with the advent of real-time payments, and I would not doubt if each BNPL account will soon have its own digital wallet attached to it that you can ‘top up’ month by month. Benefit of this to consumers = less late fees and better financial management. Benefit to BNPL = they can lend more knowing that your account is topped up (similar to a Bank’s liquidity coverage ratio ‘LCR’). Let me rephrase: if 2m Australian Afterpay customers deposit $50 into their Afterpay wallet, the company has just raised $100m. The reason this works? They are now already loyal customers - so to them, it has become ingrained in their purchasing habits + budgeting. It ticks both the responsible lending and the customer experience box.

(c) Rise of the personal finance manager ‘super aggregator’. I really think that, with the advent of every company becoming a bank (Uber, Afterpay etc), paired with a wide net of customer relationships, paired with so many repayment options for financial products (specifically BNPL - and remember, ASIC found that most BNPL customers have a relationship with more than one provider) there will be an aggregator which is the ‘one stop shop’ for all your finance needs. Frollo and Pocketbook come to mind, but I think there will be a new one pop up in no time. Throw open banking into the mix and I think PFMs will be back with a vengeance. Imagine being able to have a single view of all your finances, subscriptions, repayments, savings accounts and personal goals and automate payments across them.

I’d love to hear your comments below or in the predictions thread above. Other than that, have a fantastic break and I’ll see you next year!

All the best

Jimmy

Trivia

(a) How many countries border Croatia? One, three, or five? Also, with which country does Croatia have its longest border? (Bonus if you can name the country/countries).

(b) What country uses .pl as its internet top level domain?

(c) What 13 letter word beginning with D that means “to continue to read negative news on social media” has been chosen as the Macquarie Dictionary word of the year?

(d) Name the following logo and the product:

(e) Name the first five independent countries alphabetically that are spelled using the letter Z. (As in – the letter Z in somewhere in the name.)

Trivia Answers

👇🏽👇🏽👇🏽

(a) 5. Bosnia & Herzegovina, Slovenia, Hungary, Serbia & Montenegro. Longest border is Bosnia & Herzegovina.

(b) Poland

(c) Doomscrolling

(d) Grey Goose, Vodka.

(e) Azerbaijan, Belize, Bosnia and Herzegovina, Brazil, Czechia

The larger BNPL players will avoid being aggregated into a single view from some other super aggregator, eventually open banking will force this. I do think you will see PFM mark II with the emergence of new players with stronger value propositions than simply 'single view of my finances'. Watch this space, I'm advising one but aware of at least 2 others in various stages.

We are in the middle of a bunch of activity around the mortgage distribution space, so expect to see a bunch of different plays in different places .. within 2 years it will be clear which company/s are going to emerge as the winners in mortgage distribution long term (feels like REA/Domain playing out in the early 2000s)

The challenger BNPL will merge or die out in the next 2 years, leaving a couple of local and 1 - 2 offshores to fight it out locally

Expect to see the large non-financial retail brands get more into financial services also as their platform strategies mature

big 2021 ahead!